Business Formation Study: How are Businesses in the US Structured?

There are approximately 100 billion decisions you have to make when starting a business.

Okay, maybe that’s a small exaggeration—but you know how many critical choices demand your attention as a business owner.

One of the earliest and most important decisions you’ll make is what type of business you want to create. I’m not talking about favoring online versus physical stores or selling products versus services; this is about the type of legal form your business should take.

This determines how you’re taxed, your personal liability, how you raise money, and what happens to your business should something happen to you, to list a few considerations.

That’s why we wanted to do a deep dive on business formations today. We want to take a look at how businesses are structured in the United States and what exactly that might mean for you as you get your business off the ground.

Let’s jump in.

Disclaimer: This study is based on U.S. business formations. Apologies to our international readers out there! But we think you’ll find the information here helpful especially if you conduct business with a U.S.-based client, partner, or vendor.

The 5 most common types of business structures in the US

There are many different types of business structures out there. However, we want to take a look at the five most common types, and what that might mean for you.

They are:

- Sole Proprietorships

- Limited Liability Companies (LLC)

- General Partnerships

- C Corporations

- S Corporations

We’ll give you the pros and cons of the structure. We’ll also let you know who that specific structure might be good for.

Sole Proprietorships

Sole proprietorships are businesses that are owned and run by a single person. In a sole proprietorship, there is no legal difference between the business itself and its owner.

This is the most common way of organizing and forming a business, because it’s incredibly easy to establish and it doesn’t have to cost any money to do so. Freelancers, contractors, and “solopreneurs” often structure their business this way.

For tax purposes, all of the income, losses, and expenses you make from your business are a part of your personal income tax return. You need to report all of that to the IRS on Schedule C submitted via Form 1040.

The IRS taxes all of the profits made from business. Of course, you’re allowed to write off many expenses, including necessary purchases (e.g. office supplies), training (e.g. workshops, courses), and travel costs (e.g. flights, hotels, and conventions).

You won’t have to file a lot of documents. Depending on what service you’ll conduct, you might need to get a state or city license. And if you want to work under a fictitious name, you’ll need to register that with your state, county, or city you’re conducting business in (requirements vary depending on where you are). Other than that, though, you’ll be in the clear.

It’s also worth noting that sole proprietorships doesn’t limit your company to having just one employee. But it may require you to only use independent contractors and freelancers.

Pros

- Easy to create. With other business formations, there will be more paperwork, fees, and headaches. With a sole proprietorship, though, you won’t have to file any documents with the government.

- Taxes are simpler. Business formation types such as C corporations require you to file two separate forms of taxes: One for your business and another for your personal income tax. Sole proprietorships only require that the business owner file their personal income tax returns. Less work for you and your accountant—which is always a nice thing.

- Cheap. This is easily the most inexpensive business formation on the list, since you’re not required to file any documents unless you’re working under a fictitious name. In that case you’ll need to register a Doing Business As (DBA) with your local government. This is considered your “trade name.”

Cons

- Liability. As a sole proprietor, you’ll be personally liable for your entire business. This encompasses a number of potentially negative things such as debts or legal issues you run into while conducting your business. If you’re sued and you lose, you alone are responsible for the damages. If we had to point to the biggest downside of being a sole proprietor, this would be it.

- Continuity of business. Since you’ll be your own business as a sole proprietor, this also means that your business ends if something should happen to you (e.g. death, injury, incapacitation).

- No outside investors. Sole proprietors are not allowed to accept capital and funding from outside investors. That’s less money you could use to hire employees, create products and services, and generally grow your business.

- Can’t issue equity. Some businesses are able to issue stock options to stakeholders and employees. Sole proprietorships cannot.

Who is this good for?

Sole proprietorships are great for freelancers, consultants, and other one-person operations. It allows you to get started with your business quickly and with little cost.

If you’re looking to seek funding, however, this would not be a good choice.

Limited Liability Company (LLC)

LLCs are a very common type of business in the United States,and for good reason. Unlike a sole proprietorship, LLCs are separate legal entities from business owners. This means individual owners won’t be liable for any debts and legal issues that might arise as they run their business.

For example, if your business gets sued for millions of dollars and you lose, you won’t have to worry about your personal assets like your house, car, and savings account being seized.

It also means that the company can have several owners (also called “members”). The IRS has rules about the type of business you’re allowed to run since businesses like banks and insurance companies are not allowed to be LLCs.

There is no maximum number of owners an LLC can have either. However, many states offer something called a “single-member LLC” (SMLLC) for an LLC with just one member. So it offers you more liability protection than a sole proprietorship, but you still just have one owner.

The way LLCs are taxed depends on whether or not the owners want to enter into a proprietorship, partnership, or a corporation. Partnerships need to file a partnership tax return and corporations need to file as C or S corporations (we’ll get into that later on).

Pros

- Limited liability. You get limited protection from legal issues or debt that your business might incur. Note: That’s limited protection. It doesn’t cover everything (as we go over in the cons).

- Tax flexibility. As an LLC, you’ll be able to choose whether you’re taxed as a proprietorship, partnership, or corporation. All have their benefits and drawbacks, but the flexibility is very helpful when making your decision.

- Unlimited shareholders. You can offer stock options as an LLC to employees, investors, or stakeholders.

Cons

- Limited liability is … limited. If you don’t completely separate your personal and business expenses, you stand the chance of running into legal issues. For example, a judge can rule that your LLC doesn’t fully protect certain assets if you don’t make sure to clearly separate the two worlds. Failure to do so could cost you … well, everything.

- Fees, fees, and more fees. With a sole proprietorship, there are few fees if any. However, with an LLC, initial filing fees can vary anywhere from $45 to $500 depending on your state. Plus there are annual filing fees. One catch here though is that you can create an LLC in a state where you don’t live (e.g. a state with lower fees).

- Taxes. Proprietors and partnerships are required to pay self-employment taxes up to 7.5% on their share of the profits. S and C corporations don’t have to do this, but they do have to pay taxes up to 7.5% on their salaries.

Who is this good for?

LLCs are good for small businesses that anticipate having some degree of liability and multiple owners and/or employees. It’s a fairly easy process to set up your LLC. Plus, the benefits you have when it comes to tax flexibility and stock options make it very lucrative.

Ultimately, this is an excellent choice for anyone burgeoning small-business owner who wants to establish a company that will remain relatively contained—but offers serious growth potential.

General Partnerships

Partnerships (or general partnerships) are business entities with at least two individuals.who are owners of the business. Like a sole proprietorship, it’s very easy to set up—however, it comes with even more liability since there are more owners.

The members share all profits, debt, and liabilities incurred by the business. This can be a double-edged sword. A rising tide raises all ships—so if your partner performs well, you and your business will benefit from it. However, if your partner doesn’t, then your business will suffer.

Also there’s more liability. Everyone in a general partnership has unlimited liability on the business’s debts and legal issues. If one partner is sued by a disgruntled client and loses, then all the other partner’s personal assets like their home and savings are at risk of being forfeited. Because of this, trust is absolutely paramount when it comes to creating a partnership. If you succeed, your partner succeeds and vice versa. However, if you or your partner fails, then you both will fail.

It should be noted that a subcategory of general partnerships are limited partnerships. These are typically composed of investors and other stakeholders who don’t have nearly as much liability as general partners.

There are also LImited Liability Partnerships, which protect the partners from each other’s potential misconduct. These are great for companies that have multiple professionals acting as a single entity (e.g. law firms).

Pros

- No double taxation. General partnerships offer a very lucrative deal in terms of taxes. After all, you don’t have to pay taxes on the business’s profits. Individual partners do have to pay taxes for their personal income from the business. But the general partnership itself isn’t taxed.

- Easy to start. General partnerships are incredibly easy to form. In fact, you can form one using just an oral agreement between partners. However, we highly recommend you draft a written contract for legal purposes. Contact an attorney to set up a partnership agreement to do so.

- Less fees and paperwork. There are few to no fees incurred when creating a general partnership. There’s also less paperwork when it comes to this formation. As we mentioned, it can literally be formed through a handshake agreement (though we recommend you get it on paper).

Cons

- More liability. In a general partnership, you’re not only liable to legal issues that arise with you but your partners’ as well. Depending on how many partners you have, the chances of you running into trouble only goes up. That can put your personal assets at risk.

- No continuance. If one of the partners dies or is incapacitated then the partnership is dissolved—and with it, the business itself. This is also the case if one of the partners decides to withdraw from their partnership. If that happens, the entire partnership is dissolved.

- Sharing debt. If one of the partners secures credit for the business, the rest of the partners share in that debt. This can create for some very sticky situations, especially if one of your partners gets credit without your knowledge.

Who is this good for?

This is an option for small businesses with few to no employees, but has two or more people who want to start a small business. Honestly, it’s not the best organizational structure out there and we’d recommend going with another option like forming a corporation, an LLP, or an LLC if you can.

C Corporations

C corporations or “C corps” are separate legal entities from the business owner. The C refers to how the entity is taxed, under subchapter C in U.S. internal revenue code.

This subchapter helps ensure that C corps have double taxation. That means that the corporation itself will be taxed on profits and then the shareholders will be taxed on their dividends.

The benefit, though, is that they offer a high degree of liability protection for their owners. After all, they’re a separate legal entity. That means if a disgruntled client sues your C corp, your personal assets are unlikely to be seized.

We mentioned before too that shareholders are taxed on dividends. This is because C corps can issue stocks (and therefore stock options) to shareholders.

All these benefits come with some catches though. For one, C corps are required to have a board of directors. These are designated officers who manage the business. The board of directors are also required to have an annual meeting where they elect their officers. If you’re the founder of a C corp, you must cede control and decision-making power to the board. If that’s an important element for you, definitely take it into consideration.

Pros

- Little liability. The biggest boon of a C corporation is the fact that you’ll be protected from personal liability since it’s a separate legal entity. In fact, shareholders are typically only liable for any debt that might be incurred over the course of the business.

- Attaining capital. If you’re looking to raise funding from outside investors, C corporations are the way to do it. In fact, venture capitalists typically only fund C corporations. Why is that? Honestly, it’s because your business will have “corporation” as a part of its name. Seriously. VCs are weird.

- Continuance. If something terrible should happen to you or a founder of your business, the C corporation lives on and the work will continue. That means everyone who relies on the income brought in by the business can continue to rely on it.

Cons

- Double taxation. C corps are taxed twice. Once on the profits, and once again on the shareholder dividends.

- Fees, fees, and more fees. You’re going to have to pay filing fees each year in order to keep your corporation registered. You’ll also have to pony up a one-time registration fee.

- A lot of formalities. C corporations are required to perform a bunch of little (and, frankly, annoying) formalities such as forming a board of directors, holding annual meetings, adopting bylaws, and more. This can distract from the tasks you want to devote most of your time and energy to.

Who is this good for?

If you’re planning on going public, a C corp is a great way to structure your business formally. It also helps that you have a lot more liability protection since your business will be a separate legal entity from you.

It’s also a good option if you’re seeking funding from venture capitalists. They tend to favor corporations more than other entities because of how legitimate it sounds (I’m being completely serious; VCs are weird folks).

S corporations

S corporations are another type of corporation (and also water is wet!). Just like the previous category, the S refers to subchapter S in the IRS tax code.

S corporations are considered “pass-through entities.” That means they aren’t subject to double taxation, because shareholders report all of the corporate income, losses, and debt on their individual personal tax returns.

S corps are also notable because there are no “owners” of the businesses. Instead, there are those who own shares of stock in the business. You can have more influence over the company if you hold more stocks. However, shareholders aren’t typically the ones who run the company. Rather that’s up to the board of directors (remember them from C corporations?).

Like C corps, S corps are also required to have a board of directors elected by an annual shareholders meeting. The ones elected to the board will be the ones running the day-to-day operations.

The directors in the board also elect the officers (president, VP, treasurer, and secretary usually).

Pros

- Pass-through entity. As an S corp, you’ll be able to establish your business as a pass-through entity, which means you won’t experience double taxation. All profits and losses flow through the company and to the shareholders. This is especially lucrative if the company founders invested money into the business, since the losses can be written off in their tax returns.

- Less liability. This is another aspect S corps share with their C corp siblings. Since the business is its own legal entity, shareholders are protected from personal liability. As such, there’s a barrier to their assets being seized in the chance there’s a bad court case.

- Continuance. The transfer of ownership for an S corp is fairly simple. So you don’t have to worry about the business being dissolved or disorganized in the event or withdrawal.

Cons

- Stricter rules. There are a lot of rules that come with creating an S corp. For one, you’re limited in the amount of shareholders—you’re allowed no more than 100. You also need to be a U.S. citizen/resident or be an estate or be a specific eligible trust to be a shareholder in an S corp.

- A lot of formalities. Like C corps, you’re expected to have a bunch of formalities, such as the annual meeting of the shareholders and board of directors, as well as the adoption of bylaws.

One class of stock. As an S corp, you’ll only be allowed to have one class of stock. You aren’t allowed to have both common and preferred stock. If you do so, you could have your S corp status revoked. - Fees, fees, and more fees. Like C corps, you’ll be expected to pay a stiff filing fee from $300 to $900 as well as various legal and accounting fees. That doesn’t even get into the annual upkeep fee you’ll have to pay.

Who is this good for?

Bigger businesses that want to be protected against personal liability and double taxation. Also, this is a fit for businesses who are or are expecting a steady amount of income. Those filing and legal fees aren’t going to pay for themselves.

How are businesses in the US Structured? Stats and Facts to know

Those are the five most common types of business formations and structures you’ll see in the United States.

Let’s now dive a little deeper under the surface to see what the numbers behind them look like. Below are a few stats and facts you should know when considering the type of business structure you want to form:

Fact #1: The most popular place to establish a corporation is…

Pop quiz: What state is the home to companies such as Citigroup, JPMorgan Chase, Morgan Stanley, and Goldman Sachs?

No it’s not Wall Street. It’s not even in New York City. They’re all actually based in Delaware—at least on paper.

In fact, they actually all share a single address: 1209 North Orange Street. That’s the home of the Corporation Trust Center in Wilmington, Delaware. Here’s what it looks like.

Source: WikimediaNo, seriously. It’s true. That building that looks like a dentist’s office is actually the legal home of some of the wealthiest corporations in the world. Some 300,000 businesses are registered at the location. Other businesses “housed” there include Apple, General Motors, Google, and American Airlines.

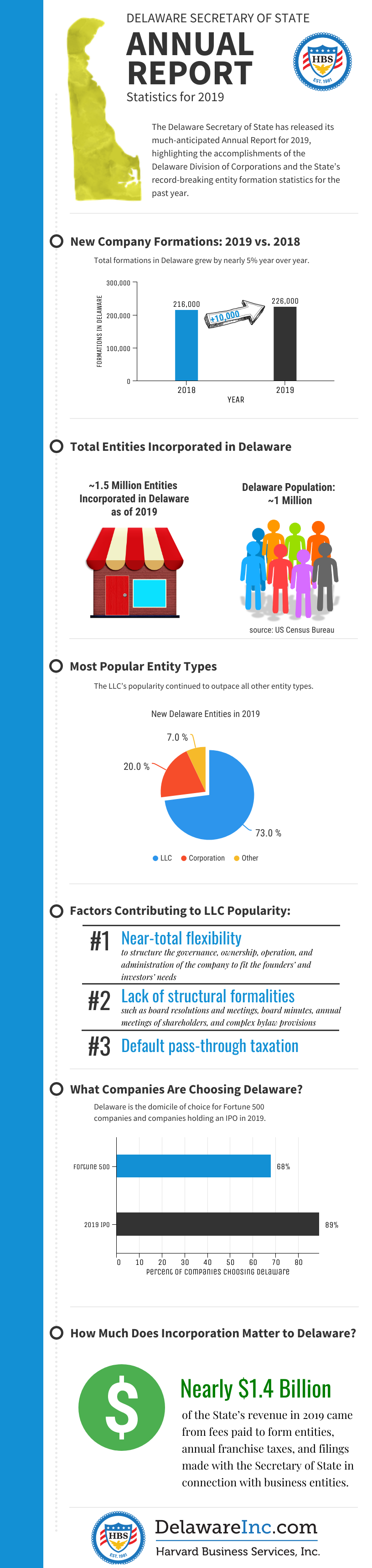

The entire state of Delaware is home to more than 1.5 million business entities. That’s more than one business to every single resident who lives in the first state (pop. 950,000). In 2019 alone, more than 226,000 businesses were formed there. The most popular of those business structures were LLCs:

Source: DelawareIncThe reason that Delaware is so popular is because of a set of tax systems and laws that have made it incredibly business friendly (in a legal way!) since the late 18th century. For example, the Delaware Court of Chancery has literal centuries of legal precedent in settling corporate legal suits. They also allow businesses to settle legal disputes with just a judge instead of a jury.

There’s also the “Delaware Loophole,” which allows businesses to declare their revenue in Delaware rather than the state where they actually conduct business. This means they avoid their state’s taxes. It should also be mentioned that Delaware doesn’t tax on a number of different things, like corporate income.

Overall, if you really want to maximize your tax advantages and join a club made up of some of the most powerful corporations in the world, Delaware is your place.

Fact #2: Sole proprietorships are the most popular type of business formation (by a large margin)

Even though LLCs are the most popular type of business formations in the most popular state for Big Business, sole proprietors are the real majority in the United States.

As of 2016, there’s close to 26 million sole proprietors in the country alone, according to the IRS. As a comparison, in 2010 there were only 23 million sole proprietors. And the number increased a TON over the years prior to then (see chart below).

Source: Tax FoundationDoes this mean you should start a sole proprietorship? Not necessarily. But it does indicate that there are some clear advantages to having a sole proprietorship over an S corp, C corp, or partnership. For example, it’s incredibly easy to start up. There are also likely going to be more in the future with the rise of the gig economy (e.g. Lyft, Uber, Postmates)

Fact #3: C corps are less and less popular each year

You can also see in the chart above that S Corps and partnerships come in second while C corporations fall in third. In fact, the number of C corps seems to be dwindling by about 60,000 C corps each year.

Source: Tax FoundationIt doesn’t take an economist to figure out why, either. Pass-through entities. S corporations, partnerships, and sole proprietorships aren’t double taxed. Therefore, they’re seen as much more lucrative opportunities for business owners to maximize their profits.

It’s also an indicator of the wider range of economic issues business owners have faced in recent years. After all, since 2009 we’ve seen two different economic recessions and disasters that have absolutely hamstrung entrepreneurs’ ability to make money. It only makes sense, then, that they’ll pursue more lucrative options.

Fact #4: 2020 is a BOOM year for business applications

Did you think that a global pandemic ravaging the world would stop people from applying for businesses?

Well…yeah, I guess I did too. But apparently that’s not the case! In fact, more businesses are being applied for than ever in the United States. 2020 has been an absolute boom year for business applications, with nearly 160,000 businesses applied for since the year began.

Source: U.S. CensusIt’s a massive increase of 38.5% compared to 2019.

Source: U.S. CensusNow the increase could be attributed to a few factors. For one, the stimulus bills passed by the U.S. government might have encouraged and incentivized a lot of people who otherwise wouldn’t have started businesses to do so.

Think about it. After you’ve been let go from your job due to the consequences of the pandemic, and the government hands you a $1,200 check, you might feel the urge to use your new time and money to start a business to get some income. Whatever the reasons, the surge of new businesses means that a post-pandemic economic boom is lying in wait.

Conclusion

There are many ways to start a business. However, the most popular way is easily sole proprietorships. Not only is it easy for you to start one but you don’t face the headaches that come with starting a corporation—such as legal and filing fees—as well as the tax disadvantages.

Whatever you ultimately choose, be sure to check back on Quick Sprout for more guidance and information on how to start your business.

Build your free WordPress website with Host2.us free hosting today!

#/media/File:1209NOrangeStreet00.jpg){kind=link}

{kind=link}